2020 AFPM Summit: Five trends to watch as coronavirus reshapes the global olefins industry

Five trends to watch as coronavirus reshapes the global olefins industry

PATRICK KIRBY, Wood Mackenzie

The coronavirus outbreak is having a transformational effect on global olefins. Supply, demand, trade, pricing, costs and margins are all being affected to the extent that it will undoubtedly reshape the wider industry.

So, what forces are defining the “new normal?”

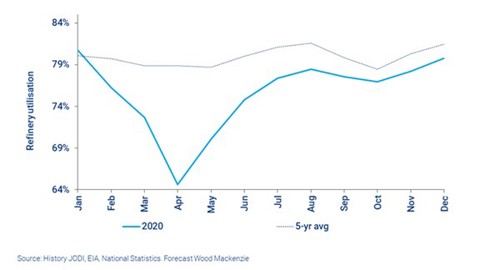

- Refinery run cuts have started—and could intensify. Reduced demand for transportation fuels has led to refiners cutting rates to manage supply (FIG. 1). The impact on olefins supply varies by region, but there is a clear domino effect.

FIG. 1. Global refinery utilization.

Olefins production is linked to the U.S. refining industry in two key ways:

- Direct propylene supply (primarily via gasoline production)

- Feedstock supply for steam crackers, converted to ethylene and propylene.

Potential now exists for feedstock limitations at refinery-integrated steam crackers, with limited options for alternative supply. Lockdown measures could disrupt refinery and steam cracker maintenance, increasing supply in the near-term, but this will have little impact on the overall effect. This situation could open up debate about the strengths and risks of further refining-olefins integration—a trend expected to grow through the energy transition.

- OPEC+ oil supply cuts will impact NGL supply. OPEC+ production cut agreements could have a sizeable knock-on effect on natural gas liquids (NGL) feedstock supply. A quarter of the world’s ethylene supply is tied to ethane-based production in locations that will reduce oil production: the U.S., Saudi Arabia, Kuwait, UAE and Russia. The full extent and location of oil supply cuts will ultimately determine the impact on petrochemical feedstock supply—and the potential for lower output.

- Feedstock inter-competition has magnified. The rapid fall in crude oil price has significantly altered global steam cracker feedstock preferences, and inter-competition is intensifying. Flexible assets will be best positioned to take advantage of near- and medium-term volatility. In the U.S., flex-crackers could have an opportunity to take advantage of butane economics relative to ethane cracking. Liquefied petroleum gas (LPG) will continue to compete with ethane. Outside the U.S., international ethane cracking is increasingly challenged in 2020 as the least preferred feedstock. Europe and Asia will see naphtha return to the preferred feedstock, at the expense of propane and butane.

- Globalization will be reassessed. The coronavirus outbreak could spark a reassessment of trade patterns, with a shift to shorter supply chains. Near-term, the low oil price impacts the competitiveness of export-oriented trade models. Feedstock, olefins and derivatives projects—and potential future expansions—are dramatically altered at current levels. Longer-term, geopolitics and enhanced perception of risk could also drive change. Increased state and government support to local industries could reduce the use of finished goods manufacturing in low-cost labor centers. Expansion in demand centers will offset the risk of supply chain disruption.

- The uncertain impact on global olefins consumption. The full impact of the coronavirus on olefins consumption is highly uncertain. The current increase in medical and packaging applications is providing a short-term demand boost, but it will be undermined by a major economic contraction.

A new Wood Mackenzie polymer demand model highlights two potential scenarios for the industry: setback and shock. Based on these scenarios, we forecast demand loss from polypropylene (PP) and polyethylene (PE) alone at between 3 MMmt and 20 MMmt.

Wood Mackenzie’s Americas Olefins Conference, set to take place on October 14th, will further delve into our base case olefins outlook and potential industry disruptors.

For more information, visit http://www.cvent.com/events/2020-virtual-olefins-conference/event-summary-b84bc59f1a8549be9e95f76f7dabafa6.aspx?RefID=HydroPro20

ABOUT THE AUTHOR

PATRICK KIRBY is a Principal Analyst for Wood Mackenzie. He joined Wood Mackenzie’s Chemicals team in 2013 as a Senior Olefins Analyst in the EMEARC region, holding almost a decade of direct experience in the petrochemical industry. In his current role, Mr. Kirby leads Wood Mackenzie’s light olefins analysis for the EMEARC region. He is regularly sought out by clients and the industry for his detailed knowledge and insight into regional olefins markets.

Comments