2020 AFPM Summit: “Refinery of the future” must consider today's demand issues

“Refinery of the future” must consider today's demand issues

ADRIENNE BLUME, Executive Editor, Hydrocarbon Processing

At AFPM's virtual Summit on Tuesday, a midday session on refinery profitability and crude-to-chemicals production welcomed Anne Huber, Senior Consultant for Argus and Keith Couch, Senior Director of Technology Sales and Integrated Projects for Honeywell UOP.

The speakers discussed the market drivers encouraging refiners to examine a departure from traditional fuels production to chemicals production. Robert Ohmes of Becht Engineering moderated the session.

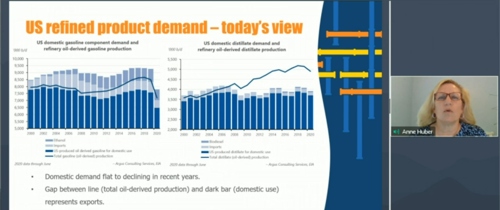

Demand impact from COVID-19. Anne Huber first discussed the overall fuel and petrochemical supply/demand pictures for the U.S. and globally. She noted that global crude supply is not a concern over the long term and that various grades of crude may fluctuate in supply based on production and demand, but that prices will sort out these movements. Huber noted that refined products demand was flat from 2016 through the ramp-up of COVID-19 in 2020 (FIG. 1).

FIG. 1. Refined products demand from 2016 through the ramp-up of COVID-19 in 2020.

"The dieselization of the U.S. is complete at this point," she noted. "Alternative fuel use can have an impact on the distillate pool, even more than gasoline. Truck fleets are a prime candidate for fuel-switching due to them having a home base." Fuel-switching competition will come from renewable fuels, electric vehicles (EVs) and other sources.

The impact from EVs on fossil fuel demand will continue to expand, but for EVs to achieve a 10% share of the U.S. vehicle fleet will require step changes in battery cost and weight, vehicle mileage, vehicle purchase costs and other factors. Growth in EV demand is driven by five key factors: purchase price, maintenance costs, range capability, vehicle usability and government regulations/subsidies.

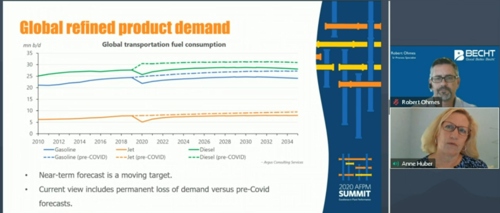

Hubert foresees a permanent loss of demand post-COVID-19, especially for diesel and gasoline (FIG. 2). Fuel demand will come under pressure from number of areas, whether from the demand side or due to competition from producers.

FIG. 2. Global refined product demand.

In the U.S., PADD 3 (Gulf Coast) refiners are dependent on gasoline and diesel exports to maintain their utilization rates. PADD 3 refiners have accounted for approximately 90% of U.S. product exports since 2019. Most of this volume heads south to Mexico, Brazil and other South and Central American countries. These exports are expected to continue due to the lack of refining capacity in South and Central American countries. PADD 1 (East Coast) refiners, meanwhile, face competition from PADD 3 refiners, as well as from refiners in Europe and elsewhere.

Petrochemicals outlook. In the U.S. petrochemical chain, polyethylene (PE) and polypropylene (PP) are the largest-volume and highest-growth areas for olefins. For steam crackers, the heart of the olefins chain, the system design is critical to determining the products that are produced. Cracker output varies significantly based on the feedstock used. PE volume is greatest with an ethane cracker and lowest with a naphtha cracker. Most regions are focusing on ethane and propane crackers.

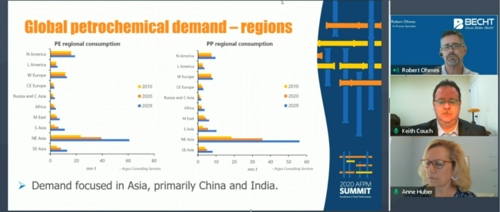

Hubert expects the COVID impact to reduce fuel supply growth through 2023 by 6%–7%, effectively canceling 2 to 2.5 years of economic growth. "Keep in mind that, in the petrochemicals world, Asia-Pacific accounts for about two-thirds of overall growth," she noted. Demand for primary petrochemical derivatives will be focused in Asia, primarily China and India (FIG. 3).

FIG. 3. Global petrochemical demand by region.

Project delays also should also be expected. "We see cracker operating rates back in the 80% range until demand catches up with capacity," Hubert said. "Regional demand for ethylene will be driven by feedstock costs, but derivatives will continue to be widely transported across regions to serve local demand." Meanwhile, the polypropylene growth rate is forecast at 4% over the next decade, with multiple supply sources competing for the same markets.

What will the refinery of the future look like? Keith Couch next talked about crude-to-chemicals operations and refinery models. Integrated refinery models compete on a global stage (FIG. 4), while refineries that produce only petrochemical feedstock from crude oil take a different path from most refiners that want to push crude into fuels. Petrochemicals integration is becoming the standard for new world-scale refinery investments; however, a future where some refineries produce only petrochemical feedstock is possible. The bottom line, Couch explained, is that "The business model has to emulate the success you're trying to drive."

FIG. 4. The growing trend of integrated fuels and petrochemicals.

Regarding the future of refining for fuel production and/or petrochemical feedstock, Couch is convinced that fuels refining has a strong future. "The refinery of the future must be flexible within certain means of technology and with regard to its business model, and it's got to be integrated and connected, such as through big data analytics," he explained.

Key technology and operations drivers. New technology innovation will focus on process intensification, bottoms upgrading and getting more from less. A number of existing assets will be repurposed to produce higher volumes of olefins and aromatics. Molecule management, optimized configurations and advanced technologies are critical for maximizing value. However, Couch also warned that higher-edge operating modes and connected-plant technologies "…only work to the degree that your business model allows them to."

Couch noted that six key concerns are driving refineries of the future: (1) putting carbon in the right place, (2) optimizing sources and uses for hydrogen, (3) reducing utilities costs and usage, (4) providing for a greener tomorrow by reducing emissions, (5) treating water as a scarce resource, and (6) driving for the most bankable project by using capital wisely. These six concerns will drive refinery and petrochemicals investments, especially for integrated plant configurations, over the next decade and beyond.

Comments