GE O&G '17: Snam CEO foresees LNG boost from 30 new markets

By Adrienne Blume, Editor, Gas Processing and Executive Editor, Hydrocarbon Processing

FLORENCE, ITALY—Near the conclusion of GE Oil & Gas' Annual Meeting 2017, Marco Alverà, CEO of Snam Group, spoke on Tuesday about fueling the future with natural gas.

Mr. Alverà named four important trends in the LNG industry:

- The influx of LNG capacity coming online

- Strategies for lowering LNG production costs

- Emergence of new LNG markets

- New uses for natural gas.

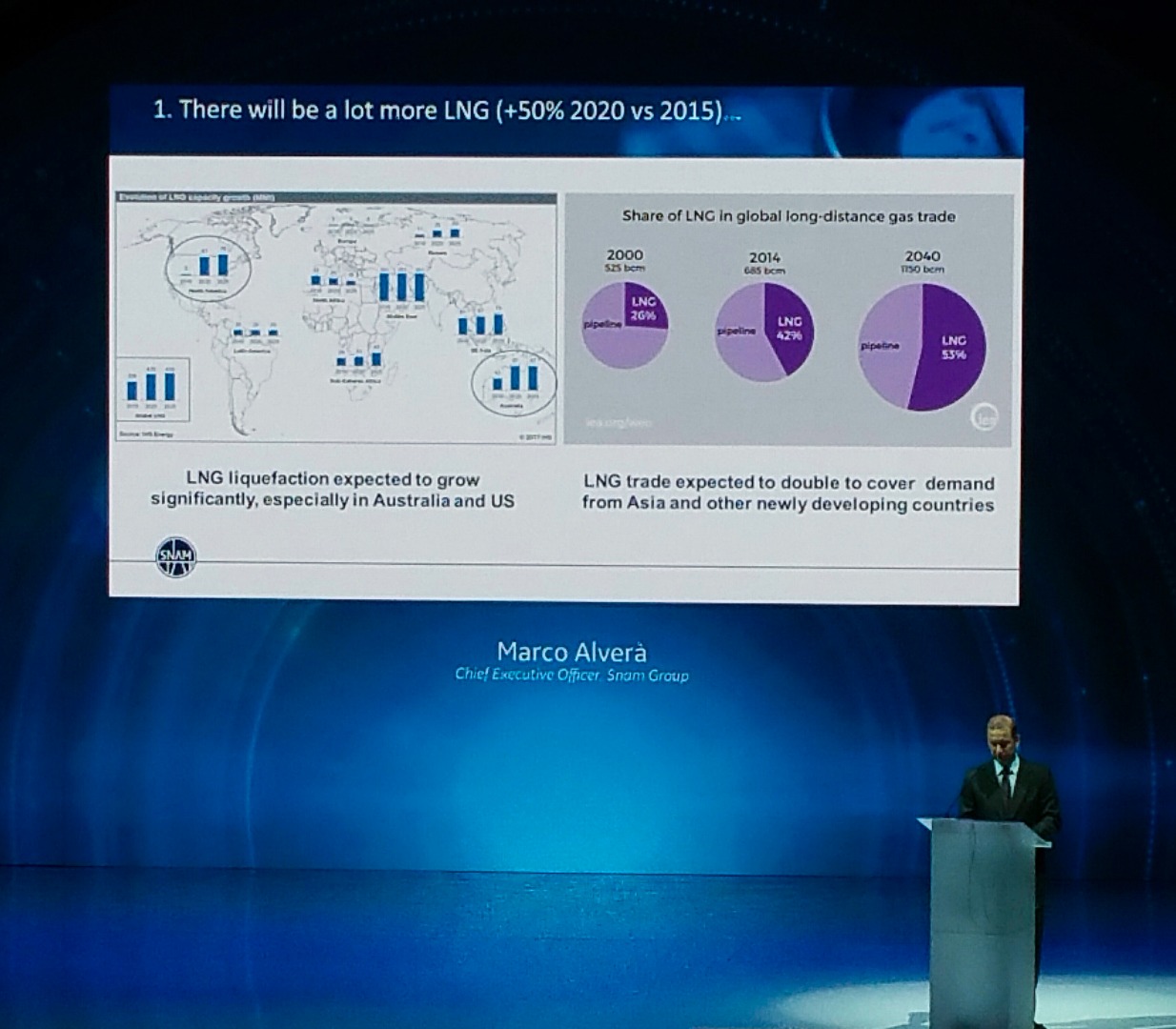

The next wave of LNG capacity. The first, and foremost, trend to watch is the startup of new LNG capacity in the next few years—a lot of it. Mr. Alverà expects 50% more LNG capacity to be in operation in 2020 vs. 2015 (Fig. 1).

However, downward pressure on global gas prices, particularly in areas where significant storage is available, will weigh on the market's ability to absorb this extra capacity during times of the year where storage is full. "LNG will become a very seasonal commodity," the CEO noted.

Reducing LNG project costs. The need exists to lower the cost of liquefying natural gas. The last decade saw an unprecedented rise in project CAPEX, Mr. Alverà said. The cost of some new projects has been more than 1,000% higher than projects carried out in the early 2000s. This steep rise in capital costs is unique to the LNG industry, the CEO noted.

Going forward, the market will take away valuable lessons from the rapid cost inflation. Efforts are presently underway to tackle this issue. Market players and analysts are examining how to bring costs down to below $500/t, and how to make LNG more competitive.

New LNG players take the stage. A third trend is the emergence of more than 30 new LNG markets over the next several years. New regasification capacity will come online in Asia—mainly China and India. Emerging markets in Asia, South America and Africa will see investments in onshore, floating LNG (FLNG) and floating storage and regasification (FSRU) projects.

These regions will also see the establishment of new gas systems. "These systems will provide significant opportunities for those involved in natural gas infrastructure," Mr. Alverà noted.

Europe also offers an attractive opportunity for LNG, although its realistic demand outlook is "flattish," the CEO said. Europe has seen a sharp reduction in indigenous natural gas production that will require an increase in gas imports of approximately 40% over the near and medium terms.

Additional gas supplies will come from the debottlenecking of national interconnections, while new supply sources will foster market integration, greater liquidity and security of supply, Mr. Alverà explained. He believes that the EU should consolidate from 27 different markets to one market. LNG must also find ways to compete directly with clean coal in Europe, the CEO said.

Innovative uses for gas. The last trend to watch is that of new technology sources and uses for gas. Mr. Alverà gave the example of biomethane, which can be produced from landfills or agricultural waste. Biomethane is fully renewable, does not add emissions to the atmosphere, supports agricultural business models and is also fairly cost-effective. "We don't yet know what the size of [this market] will be," the CEO noted. However, he said that a number of facilities presently using other fuels can be converted to run on biomethane.

Compressed natural gas (CNG) use for vehicles is another up-and-coming trend in parts of Europe, South America and Asia. Italy itself boasts 1,000 CNG refueling stations, most of which are located in the central portion of the country. CNG emits far fewer pollutants than diesel.

Lastly, interest in small-scale LNG production for transportation networks continues to increase. Mr. Alverà noted, "Significant opportunities exist in the Mediterranean [for small-scale LNG], supported by EU policies." Many ferries, for example, are installing infrastructure for LNG fueling.

The establishment of small-scale LNG production, distribution, and fueling networks offers a fully integrated natural gas supply chain. Such networks may become more common in the future to meet localized or isolated gas demand.

Comments