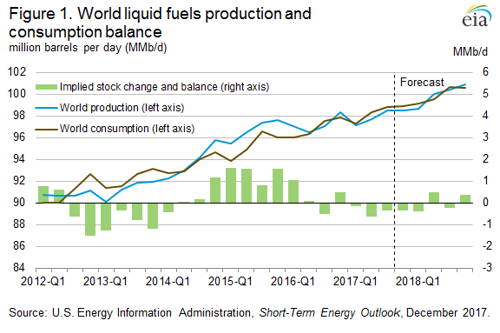

EIA forecasts a mostly balanced oil market in 2018

The US Energy Information Administration's (EIA’s) December Short-Term Energy Outlook (STEO) expects global liquid fuels demand to increase in 2018, but not keep pace with supply growth, resulting in global liquids inventories increasing modestly in 2018. STEO forecasts increasing global liquid fuels inventories by an average of 50 Mbpd in 2018, a downward revision from a 290 Mbpd inventory increase forecast in the November STEO. The change in STEO is driven by upward historical revisions to Chinese consumption and downward revisions to forecast production from countries within the Organization of the Petroleum Exporting Countries (OPEC).

On November 30, 2017, OPEC announced an extension of its agreement to reduce crude oil production through the end of 2018, which was broadly in line with both EIA’s November STEO and market expectations in the days leading up to the meeting. The non-OPEC countries that agreed to crude oil production cuts in 2017 also agreed to continue limiting output through the end of 2018. Saudi Arabia and Russia will co-chair a monitoring committee designed to assess the group’s adherence to the production targets. The group plans to reassess target production levels at their June 2018 meeting in the context of market conditions at that time. EIA estimates that OPEC crude oil production averaged 32.5 MMbpd 2017, a 0.2 MMbpd decrease from 2016 levels, and forecasts OPEC crude oil production to average 32.7 MMbpd in 2018.

Although OPEC is expected to restrain production growth, EIA forecasts that higher output from non-OPEC countries will contribute to overall growth in world liquid fuels production in 2018. The non-OPEC outlook for liquid fuels production is 0.1 MMbpd higher than EIA’s November STEO, averaging 60.3 MMbpd in 2018, 1.7 MMbpd higher than the 2017 level. This growth, together with the forecast 0.3 MMbpd growth in OPEC crude oil production and another 0.1 MMbpd increase in OPEC non-crude liquids production, results in forecast total global liquids production growth of 2 MMbpd in 2018. EIA expects that crude oil price increases in late 2017 will support growth US crude oil production to more than 10.0 MMbpd by mid-2018. Overall US crude oil production is forecast to increase by an average of 0.8 MMbpd in 2018. Canada, Brazil, Norway, the UK and Kazakhstan are also forecast to add a combined 0.7 MMbpd of growth in liquids production in 2018.

Despite higher oil prices, EIA expects global liquid fuels demand to increase by more than 1.6 MMbpd in 2018, up from growth of almost 1.4 MMbpd in 2017. Demand growth is not forecast to keep pace with supply growth, however, resulting in global liquids inventories increasing modestly in 2018. With global inventories expected to increase in 2018, EIA forecasts Brent crude oil prices will decline from present levels of more than $60/bbl to an average of $57/bbl in 2018, nearly $2/bbl higher than previously forecast in the November STEO. EIA forecasts West Texas Intermediate (WTI) crude oil prices to average $53/bbl in 2018, which is also nearly $2/bbl higher than forecast in the November STEO.

The forecast for oil prices remains highly uncertain. WTI futures contracts for March 2018 delivery, traded during the five-day period ending December 7, 2017, averaged $57/bbl. The value of options contracts currently establishes the lower and upper limits of the 95% confidence interval for the market's expectations of monthly average WTI prices for March at $48/bbl and $68/bbl, respectively. The 95% confidence interval for market expectations widens considerably over time, with lower and upper limits of $36/bbl and $84/bbl, respectively, for prices in December 2018.

US average regular gasoline and diesel prices fall. The US average regular gasoline retail price fell nearly $0.02 from the previous week to $2.49/gal on December 11, up $0.25 from the same time last year. The West Coast and Gulf Coast prices each fell more than $0.03 to $2.97/gal and $2.22/gal, respectively, the East Coast price fell nearly $0.03 to $2.47/gal, and the Rocky Mountain price fell $0.02 to $2.51/gal The Midwest price increased $0.01 to $2.37/gal.

The U.S. average diesel fuel price fell $0.01 to $2.91/gal on December 11, $0.42 higher than a year ago. The West Coast and Rocky Mountain prices each fell $0.03 to $3.34/gal and $2.99/gal, respectively, the Midwest price fell more than $0.01 to $2.86/gal, and the East Coast and Gulf Coast prices each fell less than $0.01, remaining at $2.90/gal and $2.71/gal, respectively.

Propane inventories rise slightly. US propane stocks increased by 0.2 MMbbl last week to 74.7 MMbbl as of December 8, 2017, 5.9 MMbbl (7.3%) lower than the five-year average inventory level for this same time of year. Gulf Coast and East Coast inventories increased by 0.7 MMbbl and 0.1 MMbbl, respectively, while Rocky Mountain/West Coast inventories rose modestly, remaining virtually unchanged. Midwest inventories decreased by 0.6 MMbbl. Propylene non-fuel-use inventories represented 3.3% of total propane inventories.

Residential heating oil and propane prices increase, wholesale prices decrease. As of December 11, 2017, residential heating oil prices averaged $2.88/gal, $0.01/gal more than last week and almost $0.35/gal higher than last year’s price at this time. The average wholesale heating oil price for this week averaged $2.02/gal, almost $0.02/gal lower than last week, but nearly $0.31/gal higher than a year ago.

Residential propane prices averaged $2.46/gal, $0.01/gal more than last week and $0.30/gal higher than a year ago. Wholesale propane prices averaged $1.10/gal, less than $0.01/gal lower than last week, but nearly $0.36/gal higher than last year's price.

Comments